Practically everyone knows that Social Security, as currently funded and managed, is not financially sustainable. The experts charged with overseeing Social Security have been forecasting funding shortfalls for years. The generation of workers who are providing the dollars to pay benefits to today’s Social Security recipients have been concerned for years that the program will not survive to pay them benefits. The media have reported these serious concerns: elected representatives from every level of government know there’s a problem. Unfortunately, neither the structural and systemic challenges facing Social Security for decades nor the widespread knowledge that Social Security is not financially sustainable have generated a politically persuasive demand for a comprehensive solution that would effectively fix the threats facing this indispensable program.

The current funding is insufficient to pay for the benefits currently owed. In the past 12 months, the most significant findings related to Social Security’s insolvency are a worsening timeline for trust fund depletion and sharper benefit cuts, primarily due to recent legislation and demographic shifts.

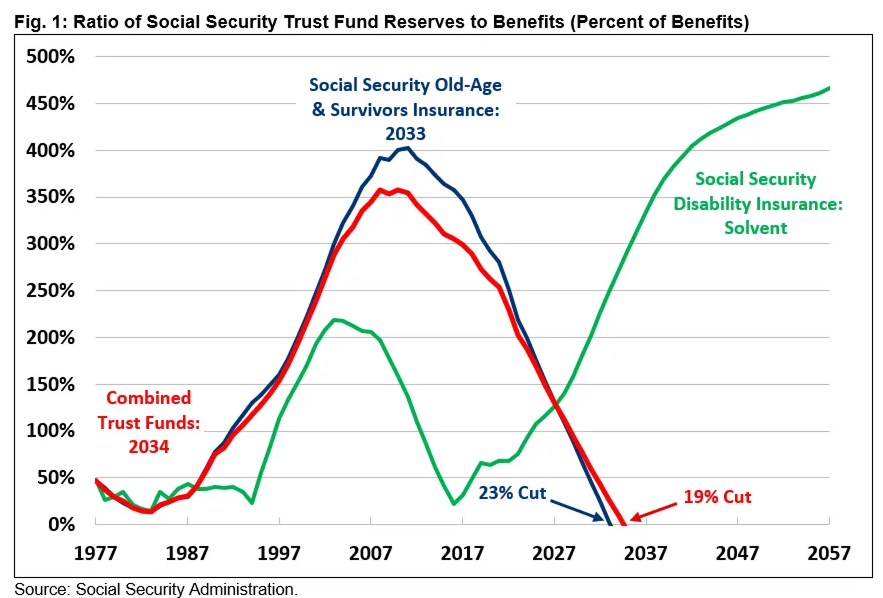

The projected date when Social Security’s Old-Age and Survivors Insurance (OASI) trust fund will become insolvent has shifted from 2033 to late 2032, following the passage of the One Big Beautiful Bill Act (OBBBA) and the Social Security Fairness Act in 2025. If nothing is done, an automatic benefit cut of about 24 percent for all recipients is expected starting in late 2032.

The OBBBA reduced Social Security revenue by cutting income tax rates for seniors, which accelerates trust fund depletion. This is estimated to cost $169 billion over ten years and widens the 75-year imbalance by 0.16 percent of payroll.

Generational equity, or intergenerational equity, is the notion that each generation of participants should fund its own benefits and not leave an unreasonable unfunded liability behind for future generations.

“Over the next 75 years, the combined Social Security trust funds face an actuarial imbalance of 3.82 percent of payroll, or 1.3 percent of GDP, the largest since 1977. A plan to restore solvency will require the equivalent of at least a 22 percent reduction in benefits for current and future beneficiaries, a 29 percent increase in payroll taxes, or some combination of the two. Because lawmakers have waited so long to act, neither eliminating the cap on wages subject to the payroll tax nor price-indexing the growth in initial benefits would be enough to restore solvency.” (Committee for a Responsible Federal Budget. (2025, June 18). Analysis of the 2025 Social Security Trustees’ Report)

The Social Security Administration’s management has become increasingly influenced by political decision-making, which threatens its stability and effectiveness. Political interference and leadership changes have disrupted oversight, accountability, and long-term planning — risking the benefits relied upon by millions of Americans.

DOGE is taking its wrecking ball to the Social Security Administration, the agency responsible for overseeing retirement and disability benefits for 73 million Americans. The cuts underway could wind up breaking critical parts of a system that millions of the nation’s most vulnerable citizens rely upon, including nearly 90% of Americans over age 65.

Axios, “Social Security in the Crosshairs,” Illustration by Sarah Grillo/Axios

Political actions affecting Social Security often provoke backlash, highlighting how entrenched the program is in national politics. Despite warnings, repeated administrative restructuring and budget adjustments continue to threaten program efficiency and beneficiary confidence.

If Social Security’s trust fund becomes insolvent, existing law would require an across-the-board benefit reduction of roughly 20%. For states like Wisconsin, this would represent a major economic shock — reducing the collective income of over 1.3 million people by $5.8 billion annually.

In Wisconsin, the 20% reduction required by existing law in the case of insolvency would reduce the income of more than 1.3 million people collectively by $5.8 billion annually.

Social Security Administration, Master Beneficiary Record (2023); Pew Research Center

The Concerned Actuaries of the United States (CAUS) will be up-dating their advanced analytics policy model to include assessments of Social Security. This brief video provides an introduction to CAUS; Board Member observations about the challenges facing Social Security and those who rely upon it; and a brief discussion about opportunities for others to provide input and feedback.

.jpg)