Well designed public policy should provide intended benefits and have the ability to calibrate designed actions, fiscal notes, and enforcement. If we want the professional principles of economics and actuarial science to keep such a policy sustained over 50 to 100 years as has been the intent with Social Security, Pensions, and Medicare then adherence with the principles of these disciplines is necessary to avoid the failure of public policy structures.

The current funding is insufficient to pay for the benefits currently owed. In the past 12 months, the most significant findings related to Social Security’s insolvency are a worsening timeline for trust fund depletion and sharper benefit cuts, primarily due to recent legislation and demographic shifts.

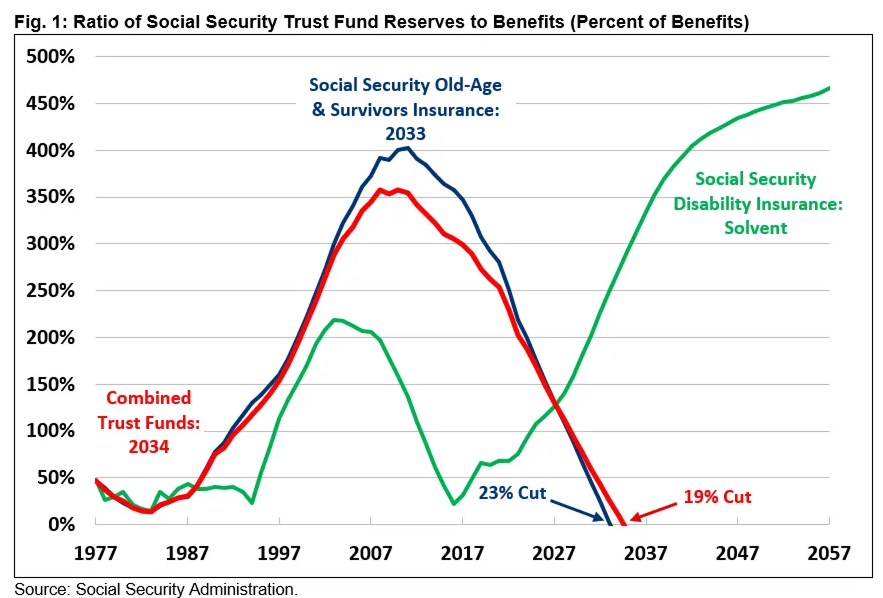

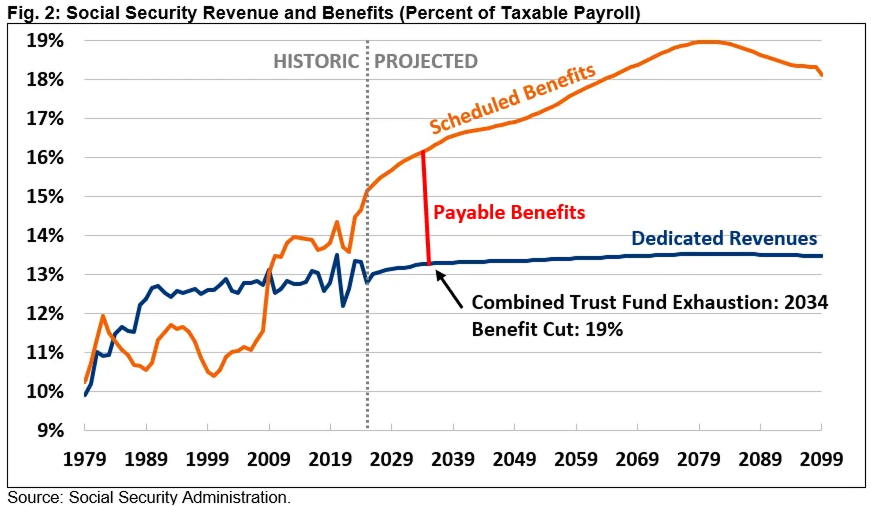

The projected date when Social Security’s Old-Age and Survivors Insurance (OASI) trust fund will become insolvent has shifted from 2033 to late 2032, following the passage of the One Big Beautiful Bill Act (OBBBA) and the Social Security Fairness Act in 2025. If nothing is done, an automatic benefit cut of about 24 percent for all recipients is expected starting in late 2032.

The OBBBA reduced Social Security revenue by cutting income tax rates for seniors, which accelerates trust fund depletion. This is estimated to cost $169 billion over ten years and widens the 75-year imbalance by 0.16 percent of payroll.

Generational equity, or intergenerational equity, is the notion that each generation of participants should fund its own benefits and not leave an unreasonable unfunded liability behind for future generations.

“Over the next 75 years, the combined Social Security trust funds face an actuarial imbalance of 3.82 percent of payroll, or 1.3 percent of GDP, the largest since 1977. A plan to restore solvency will require the equivalent of at least a 22 percent reduction in benefits for current and future beneficiaries, a 29 percent increase in payroll taxes, or some combination of the two. Because lawmakers have waited so long to act, neither eliminating the cap on wages subject to the payroll tax nor price-indexing the growth in initial benefits would be enough to restore solvency.” (Committee for a Responsible Federal Budget. (2025, June 18). Analysis of the 2025 Social Security Trustees’ Report)

The Social Security Administration’s management has become increasingly influenced by political decision-making, which threatens its stability and effectiveness. Political interference and leadership changes have disrupted oversight, accountability, and long-term planning — risking the benefits relied upon by millions of Americans.

DOGE is taking its wrecking ball to the Social Security Administration, the agency responsible for overseeing retirement and disability benefits for 73 million Americans. The cuts underway could wind up breaking critical parts of a system that millions of the nation’s most vulnerable citizens rely upon, including nearly 90% of Americans over age 65.

Axios, “Social Security in the Crosshairs,” Illustration by Sarah Grillo/Axios

Political actions affecting Social Security often provoke backlash, highlighting how entrenched the program is in national politics. Despite warnings, repeated administrative restructuring and budget adjustments continue to threaten program efficiency and beneficiary confidence.

Leaders must be aware that when they expect professionals they employ to depart from their principles of profession, they are accepting additional risk, they may be a part of corroding an intended policy, and they may be held to account.

According to the most recent Financial Report of the United States Government and analyses by Truth in Accounting and the Cato Institute:

Under GAAP, those unfunded commitments would be treated as long-term liabilities, similar to corporate pension obligations. The resulting balance sheet would shift from showing trillions in assets backed by trust funds to tens of trillions in net negative position.

In essence, applying GAAP would cause reported federal “net position” to collapse by around $110 trillion (the sum of $50T + $60T) compared to current reported figures.

In engineering, failure analysis teaches us why systems collapse and how to prevent recurrence. The National Transportation Safety Board studies near misses and crashes so that future flights are safer. We trust air travel precisely because this process is transparent and grounded in technical discipline.

Public policy should function the same way. Sound programs are designed to achieve specific outcomes and to recalibrate when experience reveals flaws. If we want Social Security, pensions, and Medicare to remain stable over generations, they must rest on the tested principles of economics and actuarial science. Policies built without those principles eventually fail.

Policy adjustments will always be needed as conditions change and assumptions evolve. The key is how they are made. When recalibrations honor actuarial and economic principles, the system remains sustainable. When they don’t—whether due to political expedience, wishful thinking, or secondary gain—the system corrodes.

Medicine reminds us of another core principle: first, do no harm. The same applies to financing care. For a free market to work, participants need simplicity and transparency. Yet today, individuals face a maze of deductibles, copays, and coinsurance that few can navigate. If insurance is meant to protect against catastrophic, unpredictable costs, should predictable, routine primary care really be called “insurance” at all?

Durable policy requires the integrity of many disciplines—medicine, economics, actuarial science, accounting, and law. When leaders ask professionals to abandon their principles, they increase systemic risk and erode public trust.

We cannot assume that “everyone is departing from principles” without consequence. Each of us has a duty to apply our professional standards to strengthen agency, simplify administration, and ensure that government is only as large as necessary to enable informed individual choice.